Q1 2026

The information in this email is private and confidential, and not intended to be shared beyond those intended recipients.

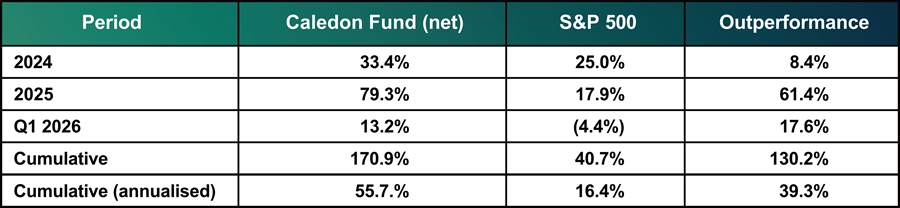

The Caledon Fund generated a net return of 13.2% in the first quarter of 2026, against a decline of 4.4% for the S&P 500. Since inception on 1 January 2024, the Fund has returned 170.9% net (55.7% annualised), compared with 40.7% (16.4% annualised) for the S&P 500 over the same period.

The quarter also saw a sharp escalation in geopolitical tension. Near-term outcomes remain difficult to predict, but the structural implications for the portfolio are, in our view, more discernible and broadly reinforcing. We address this in detail below. The performance summary is as follows:

At quarter-end, our three largest positions — Comfort Systems (7.5%), Bloom Energy (6.9%), and Siemens Energy (6.8%) — represented 21.2% of the Fund. Comfort Systems was among the strongest contributors during the quarter, benefiting from continued strong demand in data centre electrical and mechanical contracting. Argan also contributed positively, continuing to execute well on a growing backlog of power plant construction projects. Tecogen and Eos Energy detracted during the period.

Geopolitics and the Acceleration of Self-Sufficeincy

We do not attempt to forecast military or diplomatic outcomes, and we are cautious about drawing firm conclusions from events that are still evolving. For the Fund, the more important question is how the current disruption may shape longer-term structural demand. On that front, the implications are clearer: recent events reinforce, and in several cases appear to be accelerating the themes already driving the portfolio.

Security is becoming a decisive factor in the location of data infrastructure. Parts of the Middle East had increasingly been viewed as attractive sites for large-scale data centre development, given land availability, capital, and energy. Recent events have made clear that energy availability is a necessary but not sufficient condition. Hyperscalers making long-duration capital commitments now require assurance across power, regulatory stability, and operational resilience. That combination favours a narrower set of jurisdictions and supports domestic buildout in the United States.

Energy shocks strengthen the case for alternative and domestic energy sources. Even if commodity price spikes prove temporary, they serve as a repeated reminder of the strategic and economic costs of energy dependence. History suggests that energy shocks leave a longer policy legacy than the price moves that first accompany them. This supports continued investment across gas generation, renewables, nuclear, storage, and supporting infrastructure — sectors across which the portfolio has meaningful exposure.

The drive for energy independence is intensifying, not plateauing. Potential disruption to critical shipping routes highlights the exposure of oil-importing nations to forces beyond their control. We expect more countries to pursue energy self-sufficiency as a strategic objective, not merely an economic one, and to do so with greater urgency.

A recurring conclusion in our research is that major disruptions rarely reverse structural trends. More often, they compress timeframes. Energy transition, reshoring, grid hardening, and domestic manufacturing were already underway. The current environment is increasing the urgency around each.

The Infrastructure Supercycle is Broadening

We have previously described the energy infrastructure cycle as a multi-year and likely multi-decade investment theme. The first quarter reinforced our view that the demand drivers are broadening and that the portfolio is not exposed to a single source of demand.

AI-related demand has not slowed. If anything, hyperscaler ambitions continue to expand faster than consensus had expected. The cost of building a single one-gigawatt AI data centre now exceeds $50 billion. That figure illustrates why energy availability, grid stability, and domestic supply chains are not abstract constraints — they are increasingly among the decisive factors in where capital is deployed.

Reshoring and domestic manufacturing continue to drive demand. As the United States places greater emphasis on supply-chain resilience and industrial self-sufficiency, every factory brought onshore becomes a new electricity customer. Domestic semiconductor fabrication, advanced manufacturing, and related industrial buildout all require power, water, and supporting infrastructure. Several portfolio companies are direct beneficiaries through their exposure to electrical, mechanical, and general contracting work.

Critical minerals and clean-energy supply chains represent a further demand layer. Western efforts to reduce dependence on Chinese supply chains in batteries, rare earths, and solar inputs were already underway before the recent geopolitical escalation. We expect those efforts to continue — and in some cases intensify — creating further support for domestic alternatives.

The key point is that AI remains important to the portfolio, but it sits alongside a wider range of structural drivers, many of which reinforce one another.

Portfolio Implications

The Caledon Fund is, in essence, leveraged to infrastructure spending, particularly, though not exclusively, in the United States. These examples illustrate how the portfolio is positioned to benefit from multiple drivers of infrastructure demand.

Comfort Systems (FIX), our largest position at 7.5%, provides electrical, mechanical, and HVAC contracting services, essential for every large data centre, manufacturing facility, and industrial site being built in the United States. With a backlog that has grown consistently and a market where skilled EPC capacity remains structurally constrained, the company continues to benefit from both volume and pricing. While consensus estimates have risen over the past year, we continue to believe that the outer-year forecasts understate the duration of the growth opportunity.

Bloom Energy (BE), our second-largest position, provides solid-oxide fuel cells that enable reliable, lower-emission on-site power independent of the grid. In an environment where energy security matters more and grid access remains constrained, Bloom’s proposition is becoming more compelling for data centres and industrial users alike. Its strategic relationship with Oracle continues to support backlog growth, and we see scope for consensus estimates to move higher if multi-gigawatt deployments materialise.

Siemens Energy (ENR) remains one of the Fund’s largest holdings. As a manufacturer of gas turbines and a major provider of grid infrastructure, Siemens Energy is benefiting from strengthening demand for reliable power generation and grid expansion. Its backlog continues to grow, supported by robust order intake across key product lines, while the pricing embedded in newer orders suggests improving margin quality in the backlog.

Argan (AGX) continues to execute well in a market where capable EPC contractors remain scarce. As one of a limited number of firms able to build complex power plants across technologies, it benefits from both rising demand and constrained industry capacity. Speed of delivery is increasingly valuable to counterparties; Argan’s ability to deliver is, in our view, a more durable competitive advantage than the market currently recognises.

Valuation and Duration of Growth

We have written before about what we believe is a recurring weakness in consensus models: the tendency to assume relatively rapid mean reversion in growth rates within a conventional two-year forecast horizon. That approach is poorly suited to a period defined by multi-year infrastructure scarcity, long backlogs, and persistent capacity constraints.

Comfort Systems is a good example of where we think consensus may be too conservative. The Street expects revenue growth to slow from roughly 20% in FY2026 to 13% in FY2027 and 7% in FY2028. Yet the relevant leading indicators are moving in the opposite direction. Alphabet’s capex rose from $52.5 billion in 2024 to an indicated $75 billion at the start of 2025, before reaching $91.4 billion for the full year; it has since guided to $175–185 billion for 2026. Meta’s capex rose from $39.2 billion in 2024 to a 2025 guide of $60–65 billion, before reaching $72.2 billion for the full year; it has since guided to $115–135 billion for 2026. If, as management has said, Comfort’s backlog typically reflects project commitments made one to two-and-a-half years earlier, then the step-up in 2025 hyperscaler capex should be a leading indicator of stronger Comfort revenue growth in 2027 versus 2026, while the even larger step-up in 2026 capex should be a leading indicator of stronger growth in 2028 versus 2027. Consensus, by contrast, assumes the opposite pattern.

On a portfolio-weighted basis, the Fund continues to trade at approximately 20x earnings two years forward, against expected annual earnings growth of 40%+. We continue to view that as an attractive combination — and one that becomes even more compelling when the market underestimates the duration of the growth opportunity. In many cases, outer-year forecasts still assume a sharp deceleration in earnings growth that we do not believe the underlying demand environment supports.

Looking ahead

We entered 2026 with a portfolio shaped by years of disciplined research into the physical infrastructure required for electrification, industrial reshoring, and AI deployment. The events of the first quarter have not changed that direction. If anything, they have reinforced it.

America would need to expand and modernise its electrical infrastructure regardless of geopolitics. Industry was already moving toward greater supply-chain resilience. AI was already placing growing pressure on power systems, grid connections, and energy availability. What the current environment adds is urgency and, in some cases, an extension of the tailwinds supporting the portfolio.

We continue to believe that the most attractive opportunities are not necessarily in the end applications of electrification and AI, but in the physical bottlenecks that enable both. Those bottlenecks remain in place. Recent events have only increased their strategic importance.

As always, thank you for your continued trust and partnership.