Q3 2025

We are pleased to share this past quarter's investor letter with you.

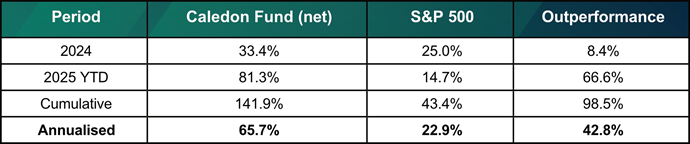

Performance

The Caledon Fund's unaudited net return for the third quarter of 2025 was 44.4% and 81.3% for the year-to-date period. Over the same periods, the S&P 500 Index returned 8.0% and 14.7%, respectively. Since inception on 1 January 2024, the Fund has delivered a net cumulative return of 141.9%, or 65.7% on an annualised basis.

At quarter-end, our three largest positions — Nebius (8.1%), IREN (8.0%), and Power Solutions International (6.4%) — represented 22.4% of the Fund. IREN (8.2%), Nebius (6.4%), and Eos Energy Enterprises (5.1%) were the top contributors to Q3 performance. We exited several positions, including Core Scientific, Enovix, and Flex during the quarter to reallocate capital toward higher-conviction opportunities, including a new position in Tecogen.

Our portfolio continues to emphasise exposure to AI infrastructure themes, with nearly 90% of the portfolio allocated to energy-related AI beneficiaries. This positioning reflects our conviction in the accelerating demand for compute power, data centers, and reliable low-carbon energy sources driven by AI adoption.

AI Infrastructure Deals – The Dawn of a Multi-Decade Boom

This quarter saw a surge in landmark deals that underscore the explosive growth in AI demand and its profound impact on the energy transition. We believe that these partnerships between tech giants and infrastructure providers are only the beginning of a multi-decade boom in AI-related capital expenditures. In this update, we explore why these deals are proliferating, their impact on our portfolio performance and valuation, and our expectations for the AI infrastructure market going forward.

In the past two months, the Fund's performance was driven by multiple high-profile AI infrastructure agreements, starting with TeraWulf's $6.7 billion, 10-year AI hosting deal with Alphabet-backed Fluidstack to provide 360 MW of capacity. Shortly after, Nebius secured a $17.4 billion, five-year deal with Microsoft to supply AI infrastructure, with potential expansion to $19.4 billion. Oracle revealed a historic $300 billion cloud computing agreement with OpenAI in its quarter earnings announcement, set to begin in 2027. Finally, on the last day of September, Meta finalised a $14 billion deal with CoreWeave to expand AI data center capacity. These deals, alongside others involving Bitcoin miners pivoting to AI like IREN's expansion of its AI cloud fleet, highlight how AI is reshaping energy and compute landscapes. This is a dynamic we discussed at length in our Q2 2024 newsletter; while we are not surprised that these deals are getting done, we may have underappreciated the extent to which the market was underestimating the speed and scale of infrastructure deployment required to support AI's exponential growth trajectory.

Toward the end of the quarter, OpenAI also announced that its Stargate project is adding five new U.S. sites, targeting seven gigawatts of capacity as part of a $500 billion, 10-gigawatt commitment. In a related blog post, CEO Sam Altman outlined a vision for a factory producing one gigawatt of new AI infrastructure weekly to reach 250 gigawatts of AI data center capacity by 2033. This ambition, if realised, would deliver 50 gigawatts annually for just one company—far exceeding the 10 gigawatts of new global data center capacity expected to break ground in 2025 alone. Against a backdrop where U.S. data center power demand stands at about 35 gigawatts today and is only projected to reach 100 gigawatts or so by 2035, such scaling ambitions underscore the urgency and scale of infrastructure needs, as well as the reluctance of most Wall Street analysts to extrapolate the current rate of AI infrastructure growth more than a year or two into the future.

The rapid advancement of AI is creating severe bottlenecks in power, data centers, and compute resources. Tech giants like Microsoft, OpenAI, and Alphabet are racing to secure infrastructure amid global supply constraints, driven by exponential growth in AI model training and inference needs. At the same time, these hyperscalers have committed to aggressive net-zero emissions targets within the next decade. As AI emerges as the largest demand driver for clean, reliable power sources, we believe that the companies that are successfully innovating and scaling to meet this demand will ultimately be big winners in the broader global energy transition.

Impact on Portfolio Performance

These announcements were key drivers of portfolio performance throughout the quarter, both directly and indirectly. Market reactions indicate Wall Street initially underestimated the scale of AI demand, leading to upward revisions in earnings across the AI supply chain. Nebius, for example, jumped 50% in one day following the Microsoft deal, while Terawulf surged nearly 60% on the back of its deal with Alphabet. IREN, which did not announce a single major contract like Nebius or Terawulf, rose more than 220% during the quarter as the market reconsidered what its large blocks of low-cost gigawatt-scale power and land located near Stargate in West Texas might be worth. IREN’s strategy of patiently funnelling bitcoin mining profits into building out its own vertically integrated AI cloud may ultimately prove to be a more lucrative strategy in the long run than pursuing larger colocation deals.

Beyond these direct ties, the deals have positive implications for companies in our portfolio that play critical roles in the data center clean energy supply chain. Bloom Energy stands out due to its strategic alliance with Oracle, deploying solid oxide fuel cells for on-site power generation. Bloom's technology provides a bridge to reliable, low-emission energy for hyperscale facilities facing grid connection delays. These fuel cells offer high efficiency and flexibility, enabling data centers to scale without full dependence on intermittent renewables or strained transmission lines. With Oracle's commitment driving backlog growth to multi-gigawatt potential and production ramping to improve margins, Bloom is well-positioned to capitalise on the surging demand for reliable clean power solutions in the AI infrastructure boom.

Eos Energy Enterprises is another company that we think will play an important role in enabling clean reliable power for data centers. The company's long-duration energy storage (LDES) solutions address a critical challenge in the AI infrastructure ecosystem by transforming intermittent renewable energy sources like wind and solar into reliable baseload power. These storage systems are particularly valuable for managing power fluctuations at data center sites, ensuring consistent uptime even during grid instability. The US regulatory and tax credit environment strongly favours domestically sourced energy storage solutions like those offered by Eos, providing significant cost advantages under the Inflation Reduction Act. We've noted rising interest from major utility customers in deploying Eos technology at scale, and management has recently hinted at discussions with a potential hyperscaler customer—a development that could dramatically accelerate the company's growth trajectory. This fits within a broader trend we're seeing, exemplified by Alphabet's investments in several LDES startups, as tech giants increasingly recognise energy storage as a critical enabler of their clean energy commitments and data center reliability goals.

Easing Concerns about Market Overheating

The Fund's strong results this quarter may prompt questions about whether the market is overheating, or worse yet reminiscent of the Internet bubble in the late 1990s. However, we caution against reasoning by analogy, which can lead to faulty conclusions when comparing different technological eras. Thinking from first principles actually leads us to the opposite conclusion - unlike the dot-com bubble where many companies lacked viable business models, today's AI infrastructure boom is driven by tangible, accelerating demand that outpaces supply. While our investment decisions are always anchored in valuation discipline, our deep focus on the entire AI ecosystem provides unique insights into growth potential and the value of technology and intangible assets that traditional metrics might miss. For instance, we recognise that "time to power" - the ability to quickly secure and deploy energy resources - represents an increasingly valuable competitive advantage that is often underappreciated in conventional financial models.

On a granular level, we see structural issues with consensus estimates for some of our portfolio companies such as limited analyst coverage, which has led to significant upward revisions over the past year—in some cases exceeding 50%. Analysts typically model substantial growth deceleration within the next two years, an assumption we strongly question if scaling laws continue to hold. These empirical laws suggest that AI performance improves predictably with more compute, data, and parameters, fuelling continued exponential growth rather than linear progress. In a scenario of sustained rapid growth rates, time to power becomes paramount, making our investments in secured power appear significantly undervalued.

Our valuation approach avoids anchoring to near-term earnings, focusing instead on multi-year potential in bottlenecks where companies trade at attractive multiples on future cash flows. Based on our internal estimates, the average earnings growth rate across the portfolio sits at about 40%, more than twice that of the S&P 500. While the portfolio’s forward earnings multiple has expanded beyond the market average, when we look two years out the average valuation is roughly 20x earnings, in line with estimates for the S&P 500. We think that significantly higher growth warrants higher valuation, and we see a long runway ahead. While it is hard not to be pleased with the shape that the portfolio has taken since launch and the subsequent outperformance, we strive not to be complacent. We also continue to monitor a deep bench of companies for opportunities to enhance the Fund's valuation and growth profile.

Expectation for Larger Deals Ahead

We anticipate even larger infrastructure deals as AI growth trajectories point to exponential scaling. Drawing on the Jevons Paradox—as efficiency improves, total resource consumption often rises—we expect AI to drive surging demand for energy and infrastructure. Through this lens, there simply may not be an upper limit on demand for artificial intelligence in the long run, but the physical challenge of securing sufficient power, cooling capacity, and transmission infrastructure will remain the primary constraint on AI growth for the foreseeable future.

If Sam Altman's vision of 250 gigawatts by 2033 materializes—and other hyperscalers like Microsoft, Meta, and Google pursue similar ambitions—we could be witnessing the early stages of an unprecedented transformation of our energy infrastructure. In a world where 90% of economic activity revolves around turning electrons into intelligence, the implications for the energy supply chain would be profound. We expect to see entirely new categories of companies emerge across the value chain: from specialised transmission developers and next-generation nuclear startups to AI-native energy storage providers and integrated cooling systems manufacturers. The companies that can most efficiently deliver reliable, low-carbon power at the necessary scale will command significant premiums.

Our Approach and Outlook

We invest where long-term demand meets limited capacity, and where structural barriers protect capable operators and support attractive returns. That often leads us to bottlenecks: critical parts of the energy system or supply chain where AI is amplifying pressures. As we look ahead, we are confident in the long-term potential of our investment strategy, grounded in structural trends like re-industrialisation and energy security. We maintain a sober view of challenges, such as geopolitical tensions.

We appreciate your ongoing support and referrals and welcome the opportunity to discuss expanding your investment in the fund.

Thank you for your support. Please feel free to reach out if you have any questions; we value your thoughts and engagement.