Q4 2024

The Caledon Energy Transition Fund returned a net unaudited return of 5.8% in USD net of fees in Q4 2024 and 33.4% for the full year. Over the same periods, the S&P 500 Index returned 2.7% and 24.9%, respectively.

While we are encouraged by the Fund’s returns since inception, it is important to acknowledge that this level of performance may be difficult to replicate consistently. We are focusing on the right areas, fishing in the right pond, but it is unrealistic to expect this "catch rate" to continue indefinitely. As such, we remain committed to our disciplined investment process, and we will continue to seek out the most promising opportunities while maintaining realistic expectations for future returns.

This quarter’s update explores two key themes shaping the energy landscape. We consider Nvidia’s role in accelerating the energy transition and we also examine the growing importance of natural gas in meeting the US's increasing energy demands while supporting the transition to cleaner sources. We recently added several direct beneficiaries of this trend, including Argan which stands uniquely positioned as a critical engineering, procurement, and construction (EPC) partner for both natural gas and renewable energy projects.

As we look ahead, we are confident in the long-term potential of our investment strategy. We appreciate your ongoing support and referrals and we welcome the opportunity to discuss expanding your investment in the fund.

Thank you for your support. Pease feel free reach out to us if you have any questions, we value your thoughts and engagement.

Sincerely, Brian, James and Will

Strong first-year results

Our strong first-year results are particularly encouraging as 2024 proved to be a difficult operating environment for most energy transition funds, with the S&P Global Clean Energy Index down more than 25% for the year. While we are optimistic that the world is indeed on track to transition to a low-carbon future, we also maintain a sober view of renewable supply chain challenges, such as material and manufacturing constraints, grid capacity and interconnection queues, and geopolitical issues.

For example, despite an acceleration in demand growth for clean energy in 2024 driven by a boom in AI infrastructure investments and very supportive federal investment tax credits, our view is that bottlenecks in skilled labor, the grid interconnection queue, and capital equipment with long lead times, such as transformers, effectively capped the amount of utility solar generation that could be added in the U.S. This coincided with excess production capacity tipping the market for solar modules and related components into oversupply.

As such, we avoided adding stocks from the underperforming solar sector to the portfolio in 2024 and enjoyed positive contributions from companies addressing these bottlenecks, including Hammond Power Solutions, the North American leader in dry-type electrical transformers, and Quanta Services, a leading provider of design, construction, and maintenance services for electric power transmission and distribution infrastructure.

Nvidia's Role in Accelerating the Global Energy Transition

Nvidia was a major contributor to the fund’s annual performance, as the stock rose 144% from our entry price and remained a core holding throughout the year. The stock’s exceptional gain was driven by even more exceptional earnings growth of 234%, and we continue to hold given its attractive growth profile and undemanding valuation of less than 30x next year’s earnings.

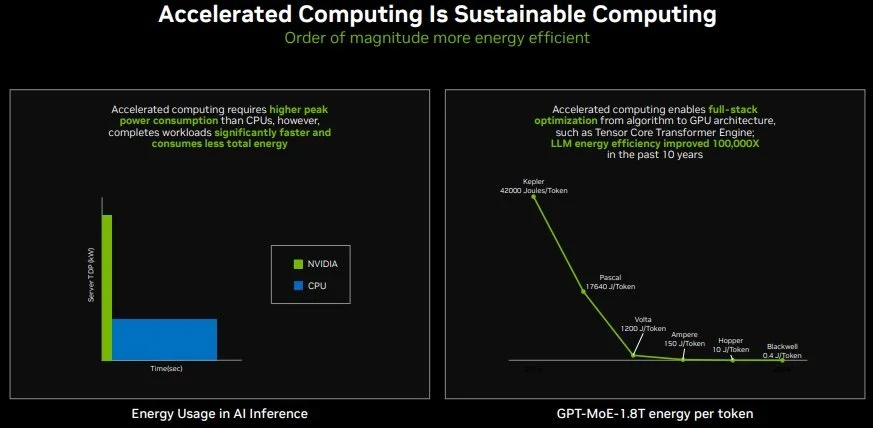

While the stock may not find its way into many energy-related funds, we believe that Nvidia has emerged as a critical enabler of the global energy transition by revolutionising the computational architecture that will make decarbonisation possible.

Over the past two decades since recognising the potential of the GPU as a general-purpose computing platform, Nvidia has forged its own path to develop a complete technological ecosystem of hardware, networking and software that dramatically outperforms traditional CPU architectures in energy efficiency and computational capability. The last generation of Nvidia’s GPU servers reduced per-unit energy consumption by up to 95% compared to legacy CPU servers, and the next-generation Blackwell servers are reported to offer another 5x improvement in performance.

As data centre operators replace their legacy infrastructure with Nvidia servers, they are realising significant energy savings for existing operations. By making computation exponentially more efficient, Nvidia is also enabling applications that will accelerate the energy transition such as AI-driven climate modelling, advanced grid management, and autonomous driving software.

Jevons Paradox

In an ideal world, Nvidia’s more efficient computation might allow us to use less energy and transition away from fossil fuels a bit faster. In the real world, we are once again observing the Jevons paradox, which posits that when technological progress increases the efficiency with which a resource is used, the falling cost of use increases the overall demand for that resource.

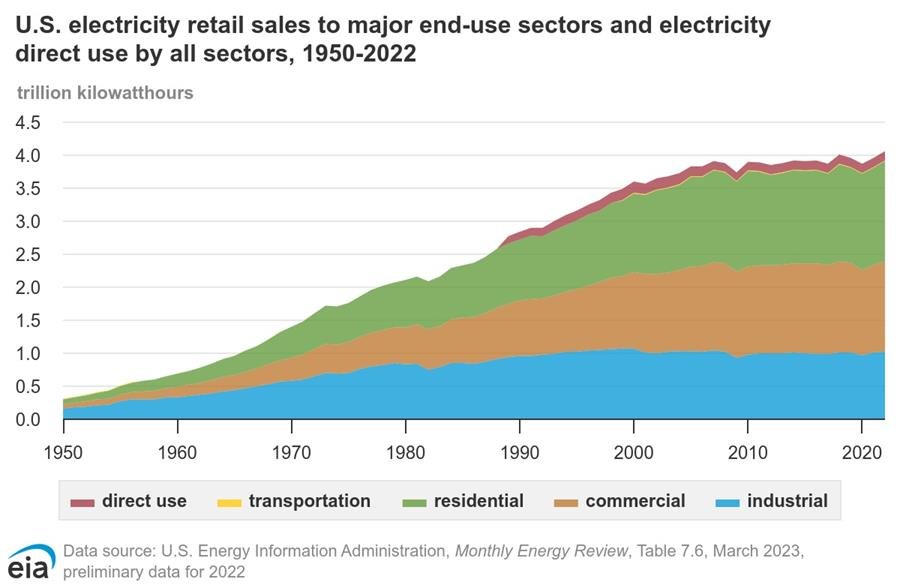

The ongoing reduction of computing costs is enabling the training of larger and more powerful AI models, which are proving to be increasingly valuable to users as they improve. As scaling laws continue to hold (more compute + more data = predictably better results), it would seem that we are caught in a cycle that will necessitate an exponential buildout of AI training and inference infrastructure, which in turn is driving exponential demand for power. Total data centre power consumption in the U.S. is now expected to rise from 2% of total demand in 2022 to potentially 20% of total demand in 2030, requiring an extreme gear shift in new power generation construction following 15 years of near-zero overall electricity demand growth.

The Inevitability of Natural Gas

Last year began with a healthy dose of clean energy optimism in the U.S.: IRA tax credits and the DOE Loans Program promised to accelerate domestic supply chains for renewables, and hyperscalers were making bold sustainability commitments for future data centre construction. Yet as the popularity of Generative AI mushroomed and data centre power demand estimates continued rising, a stark reality emerged—renewables alone cannot sustain the 24/7 computational requirements of the emerging AI economy, while new nuclear is perpetually a decade away.

This strategic inflection point has precipitated a pragmatic pivot toward natural gas as the critical backstop for data centre power architecture—a solution offering immediate reliability, established infrastructure, and a lower-carbon pathway compared to traditional alternatives.

As hyperscalers and enterprise players grapple with the dual imperatives of reliability and sustainability, natural gas has carved out a unique position at the intersection of these requirements. The technology sector's voracious appetite for power, particularly amid the AI compute boom, has exposed the limitations of grid infrastructure in key markets, pushing operators toward hybrid power solutions that can guarantee 24/7 uptime.

Natural gas infrastructure, with its established supply chains, scalable deployment capabilities, and lower emissions profile compared to diesel generators, has emerged as a pragmatic bridge technology. The ability to rapidly deploy gas turbines or fuel cells, coupled with the potential for renewable natural gas (RNG) integration, provides data center operators with a flexible pathway to balance their immediate reliability needs against longer-term sustainability goals. The Fund has recently added several direct beneficiaries of this trend, including Argan.

Argan (AGX) - Powering the AI Boom

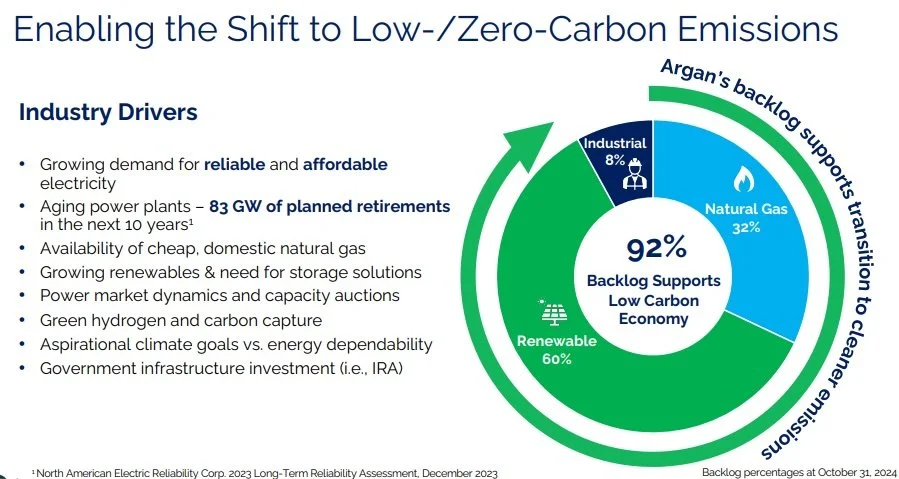

Argan stands uniquely positioned as a critical engineering, procurement, and construction (EPC) partner for both natural gas and renewable energy projects. As one of only a few companies with the capabilities and experience to build all types of complex power facilities, Argan is in a perfect position to capitalise on the growing energy demand from AI data centres.

The company's disciplined management has maintained a remarkable track record of cost control, avoiding losses on contracts for 16 consecutive years while deliberately expanding beyond natural gas into solar, wind, biomass, and waste-to-energy facilities. After surviving and learning to thrive through the lean years of natural gas power plant construction, the winds are now blowing back in Argan’s favor in a big way.

In the most recent quarter, Argan’s revenues grew 57% year over year and operating income grew 286% on the back of much stronger gross margins in the Power Services segment. The company’s backlog is 60% renewable and 32% natural gas projects, not including a Letter of Intent for a 1200 MW gas power project in Texas, which is rapidly becoming the epicentre for the AI Infrastructure buildout due to the availability of large amounts of land, water, and a mix of renewable energy and cheap natural gas.

We believe that the two analysts who cover the stock have been slow to update their models following Argan’s stellar results, as the company is already operating at a $1B sales run rate yet next year’s sales consensus sits at only $900m.

Just two days into his presidency, Donald Trump has pledged rapid approvals for new power plants for AI under a national energy emergency declaration and announced support for a $500B OpenAI Project Stargate centred in West Texas.

Given the wave of money flowing into the sector as data centre operators scramble to bring their own power online in the race to scale their AI ambitions, we think Argan’s sales and margins will come in significantly higher than consensus over the coming years. Annual additions to grid capacity are expected to grow from about 50GW in 2024 to 250GW-300GW by 2030.

By our estimate, Argan shares are trading at roughly a market multiple on next year’s earnings, with significantly higher earnings growth of 30%+ through the end of the decade.